Selection Discipline

The belief that private markets reward access is not wrong. It is simply obsolete.

A decade ago, knowing the right intermediary, being present in the right city, receiving the deck before the broader market — these were structural advantages. They compounded quietly into returns.

That compression is complete. The Asian brokerage landscape has professionalised. Digitisation has distributed deal flow at scale. What was once proprietary is now broadly shopped, and broadly shopped is indistinguishable from public. The room is no longer closed. The advantage of being in it has gone with the door.

What remains — and what the market has not yet priced — is the cost of not being able to leave.

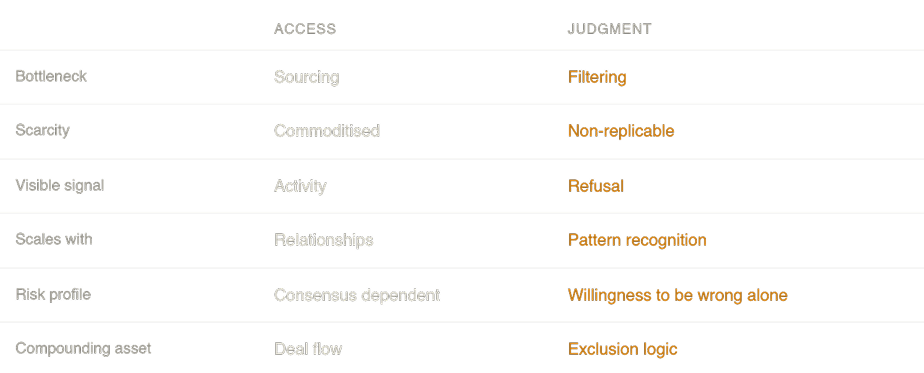

Every major allocator is currently drowning in decks. The volume is not a sign of opportunity. It is a sign that sourcing has ceased to be the bottleneck. Capital fails in this environment not because it lacks access but because it lacks the internal operating system to refuse. The filtering problem has replaced the sourcing problem, and most institutions are not structured to solve it.

Filtering is not a process. It is not a checklist or a scoring matrix. It is the capacity to hold a judgment — privately, without consensus, without the validation of comparable transactions — and act on it or not act on it with equal discipline. That capacity does not scale. It cannot be outsourced to a consultant whose incentive is to deliver market consensus and avoid career risk. It cannot be approximated by a model whose inputs are the same inputs every competitor is using.

Judgment is the identification of what to ignore. In a market saturated with signal, the most consequential part of any investment process is the exclusion logic — the account of why the other ninety-nine versions of a trade were declined. That account is where intelligence lives. The decision to invest is merely its output.

High-velocity signalling has become the visible symptom of fee dependency. Announcements, activity, presence — these are the performance of access in a market where access no longer differentiates. The institutions that signal most are often those most reliant on the appearance of motion to justify their position in the capital chain.

Quiet capital operates differently. It accumulates pattern recognition over years without announcing it. It records observations that will not resolve into positions for months or longer. It tolerates the discomfort of appearing inactive in cycles where activity is mistaken for rigour. And when asymmetry becomes undeniable — when the basis is right, the structure is clean, and the exclusion logic holds — it moves without preparation, because the preparation was already done.

The interval between recognition and action is not delay. It is the work.

High-velocity signalling has become the visible symptom of fee dependency. Announcements, activity, presence — these are the performance of access in a market where access no longer differentiates. The institutions that signal most are often those most reliant on the appearance of motion to justify their position in the capital chain.

Quiet capital operates differently. It accumulates pattern recognition over years without announcing it. It records observations that will not resolve into positions for months or longer. It tolerates the discomfort of appearing inactive in cycles where activity is mistaken for rigour. And when asymmetry becomes undeniable — when the basis is right, the structure is clean, and the exclusion logic holds — it moves without preparation, because the preparation was already done.

The interval between recognition and action is not delay. It is the work.

Performance in Key Markets

Across Asia Pacific, hotel performance varied across gateway cities. Tokyo posted occupancy above 80 percent, slightly below pre-pandemic levels, while average daily rates (ADR) exceeded 2019 benchmarks. Singapore's occupancy remained stable, with ADR surpassing pre-pandemic levels but declining slightly from the previous year. Sydney's occupancy approached 80 percent, with flat ADR trends, while Bangkok hotels recorded ADR significantly above prior peaks despite tourist arrivals dropping 6.3 percent year-over-year in the first seven months.

Participation in competitive processes where access is the only barrier to entry produces a specific kind of return: the market return, achieved at above-market cost. Beauty contests select for the most aggressive underwriting, not the most accurate. Winning them is often the first evidence that something has been missed.

The principals who understand this are not looking for a manager with relationships. They are looking for a manager with a demonstrable record of refusal — a visible history of what was declined and why. That record is not a marketing asset. It is the only evidence that judgment is operating independently of deal flow.

Access gets you into the room. Intelligence tells you when to leave it. In a mature market, the second capability is the rarer one, and the only one that compounds.